Current Economic Scenario – Part III

Last two blogs talked about the current situation of Indian Economy, here we will be talking about what happens if one of the Components of our economy changes.

*This scenario is very unlikely looking at the current situation and policy actions.

-Change in Crude Oil Prices

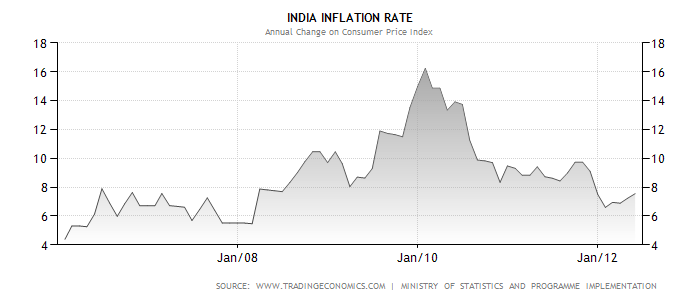

A further decrease in crude oil prices would be the most fortunate thing that could happen to revive the economy. This would mean that the supply side pressures get eased automatically reducing the inflation rate (disinflation) and thereby also increasing the demand for other industrial products and reviving the GDP growth rate marginally.

Investment opportunities if the Oil Prices Reduce:

An increase in crude oil prices with no change in currency exchange rate would be an economic disaster for the country, creating an upward inflationary spiral and reducing GDP to a great extent i.e. a situation of severe stagflation. It is very important for the Economic Bodies to react before any of these happen as a key to this problem has not been found till now and could lead to a severe depression.

Last two blogs talked about the current situation of Indian Economy, here we will be talking about what happens if one of the Components of our economy changes.

- Appreciation/Depreciation of rupee and its effects

This suggests that the most favorable scenario for the economy would be of Rupee Appreciation. Here, it is important to note that in an ideal scenario (Good GDP Growth rate, controlled inflation measures) Foreign Domestic Investment i.e. Foreign Investment in India increases with the weakening of rupee (more rupee for 1$) but in current scenario it is very important to infuse confidence into the Foreigners regarding Indian Economy.

Let’s say if You and I have got 1 billion dollars to invest than a rupee conversion rate would not matter as much as a prospective return on our investment which is indicated by a good GDP growth rate.

Investment opportunities if the Rupee appreciates:-

- Buy Govt. bonds as the yields will most likely decrease (due to decreasing inflation), increasing the Bond’s price.

- Buy the stocks of cyclical industries (industry which do well in good economic times). Example: Auto industry, Infrastructure industries, Luxury Goods industry, etc.

Investment opportunities if the Rupee depreciates:-

- Buy stocks of non-cyclical industry like staple goods, agriculture, etc. as the demand for these goods will increase with the ever-rising population.

*This scenario is very unlikely looking at the current situation and policy actions.

-Change in Crude Oil Prices

A further decrease in crude oil prices would be the most fortunate thing that could happen to revive the economy. This would mean that the supply side pressures get eased automatically reducing the inflation rate (disinflation) and thereby also increasing the demand for other industrial products and reviving the GDP growth rate marginally.

Investment opportunities if the Oil Prices Reduce:

- Buy Govt. bonds as reduced inflation would mean a decrease in require yields and an increase in bond prices.

- Buy stocks of non-cyclical industries as only a reduction in oil prices with other scenario unchanged is not supposed to revive the economy substantially.

An increase in crude oil prices with no change in currency exchange rate would be an economic disaster for the country, creating an upward inflationary spiral and reducing GDP to a great extent i.e. a situation of severe stagflation. It is very important for the Economic Bodies to react before any of these happen as a key to this problem has not been found till now and could lead to a severe depression.